Recently I read this report titled “M&A—To What End?” written by The Advisory Board Company. Although it was published in 2014, it provides good insight into the ongoing merger and acquisition (M&A) activity in the U.S. healthcare market.

There are several observations that I think are worthwhile sharing.

The motivation behind M&A

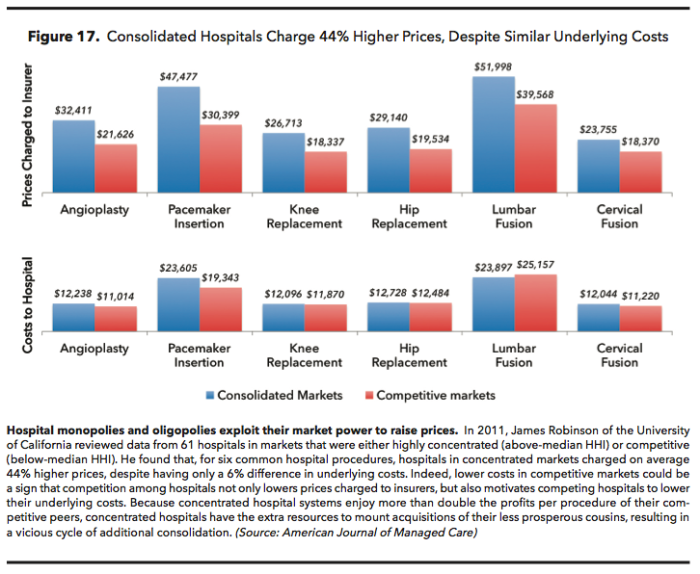

Historically, the most common reasons cited for M&A activity are: 1) the consolidated provider’s ability to demand higher prices for delivered services; and 2) the consolidated provider’s ability to secure larger referral volume. The following study by Jamie Robinson of the University of California provides empirical evidence for the first above-mentioned reason.

Therefore, it was quite interesting to read the following statement and the associated chart in the Advisory Group report:

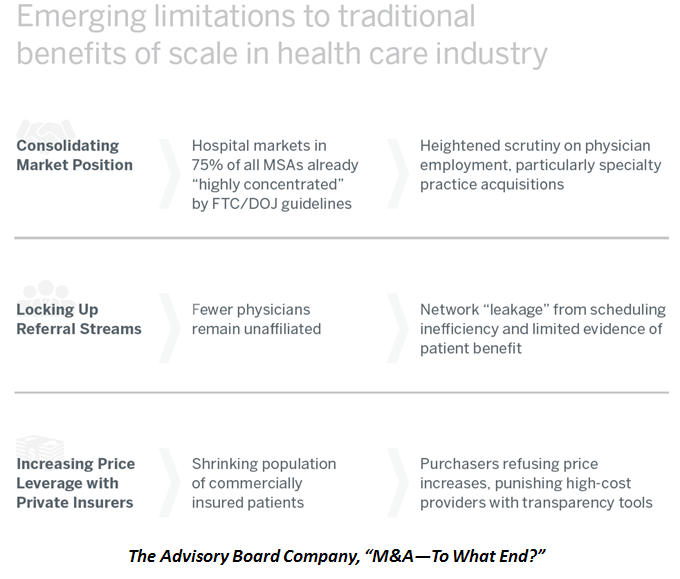

“These benefits of scale are increasingly hard to come by as the health care industry evolves and matures. Still, we see boards and management teams, from the smallest private practices and community hospitals to the largest for-profit chains, continuing to narrowly focus on scale as the primary motivation for M&A. They are asking each other, and asking us: “How big is big enough?” But these days, “How big is big enough?” is a worthy but insufficient question. Size alone, and size’s legacy benefits, will not be enough for health systems to grow profitably.

Cost-savings Opportunities

The report claims that the perceived economies of scale—that should deliver cost-savings to the merged organizations—exist, but it is very hard to capture them due to “… institutional inertia, pressure from stakeholders, and the sheer magnitude of the task…”.

The following chart is particularly interesting. It ranks different cost-savings opportunities pursued by the merged organization.

As you can see, Radiology Services represent the first clinical domain which is targeted by the merged organizations once the back-office’s economies of scale are achieved.

I find this particular ranking to be sensible. In contrast to other clinical domains, the imaging informatics industry has very mature and standardized clinical IT solutions that can scale to serve merged organizations and provide quick wins during post-merger clinical and IT integration.

Our clients are frequently growing their Radiology services through M&A and affiliation activities. The current state-of-the-art of the imaging informatics market, such as the implementation of VNA and Enterprise Viewer solutions, coupled with existing Image Sharing methods, enables them to abstract the complexities of multiple PACS systems (across multiple joined organizations) to realize both consolidated IT and clinical benefits.

As always, comments, opinions, and insights are welcomed.

Nice! Sure is hard to truly gain efficiency.

On Thursday, January 28, 2016, Don K Dennison wrote:

> genadyknizhnik posted: “Recently I read this report titled “M&A—To What > End?” written by The Advisory Board Company. Although it was published in > 2014, it provides good insight into the ongoing merger and acquisition > (M&A) activity in the U.S. healthcare market. There a” >