Acknowledgements: I would like to sincerely thank Dr. Alex Towbin (@towbinaj), Ryan Fallon, and Jason Nagels (@jaynagels) for their time to review this information and provide valuable input.

Important Note: This article is in no way intended to dissuade organizations from sharing imaging exam data. As described within, there are many benefits to everyone, and sharing of imaging data should be consider a best practice. This article is intended to explore how vendors charge differently for storing imported imaging data in their systems.

The sharing of imaging exams across different enterprises has long been of value to patients and healthcare systems. From teleradiology, patient transfers, consults, treatment planning, to other scenarios, avoiding the repeat of an exam by sharing existing ones lowers costs, minimizes stress and frustration on the patient (and their family), and avoids any unnecessary radiation exposure.

As technology and reliable Internet has evolved, the norm of printing film, then exporting digital exams to portable media (CDs, DVDs, USB drives, etc.), has given way to cloud-based image sharing solutions. With these solutions acting as a secure broker among enterprises, imaging data can be easily moved from one organization to another. Patients can even upload their exam data using a webpage.

And while the managed movement of imaging data from one organization to another has become much easier and more common, the importation of the data to systems, like the PACS, at the destination enterprise often still requires some manual activity to get the exam data acquired at another enterprise to include all the unique data identifiers used at the destination enterprise.

The costs of the above activities are all well understood by imaging professionals, but there is another aspect that is less understood: Does the receiving imaging IT system vendor charge for imported exams?

Imaging Exam Acquisition Revenues and PACS Costs

In most jurisdictions (with private or public funded healthcare), a fee is paid by the payor for each imaging exam performed. This fee, commonly called the Technical Fee (or TechFee) in the U.S., is intended to compensate the health provider for the labor, equipment, consumables, facilities, IT systems, and other resources required to perform the exam and manage the resulting data. The TechFee amount will vary among different procedures and payors.

Note: A Professional Fee (ProFee) is also billed, but these funds may go to pay the Radiologist group, if they are not directly employed by the health system. So, even if an imported exam is read (for example, as an “over read”) and a ProFee bill generated, in some cases, the health system paying for the PACS does not receive any revenue (but do incur costs, as detailed below). Not to mention, ProFee billing for over reads can be unpopular among patients and referring physicians, as it increases overall cost of care.

It is common for PACS vendors to charge a software license for the use of the solution. The commercial model may vary between a licensed annual exam total allowed or a per use fee, but in most cases, the more exams that are acquired and stored by the organization, the more the vendor is paid. This is generally accepted as fair by both vendors and health system buyers.

Where there can be variability in vendor agreement terms is in deciding which exams are counted when determining compliance with the license terms or fees for usage. As the health system receives a TechFee for any exams they acquire, both vendor and health system provider are generally in agreement that these exams should count towards the software license.

But what about imported exams?

Some vendors treat all exams – acquired and imported – as equal and they are both included in the license compliance or usage calculations, even though the health system typically receives no compensation for imported exams. Some vendors may charge a lower fee for imported exams, while others include terms in the agreement that specify that only exams acquired by the health system, and not imported exams, are counted.

If multiple applications are involved – for example, a cloud-based image sharing solution, a local system for reconciling the imaging data with a local order, the PACS, and a Vendor Neutral Archive (VNA) – there may be the terms of solution’s software licenses to review and consider.

Do you Need to See the Images or Have the Images?

Before exploring how imaging IT vendors may count exams when determining system usage for software license calculations, let’s discuss some different ways in which imaging data are accessed and shared.

Image Viewer

Some enterprises provide a web-based image viewer, often as part of a referring physician or patient portal, to allow authorized users to see and navigate images and results. Cloud-based image sharing solutions also allow images temporarily stored to the solution to be viewed by authorized users. Similarly, Health Information Exchanges (HIEs) that support image data exchange usually also provide an image viewer to see the images. Common among all of these approaches is the ability to see and interact with the images without having to move the DICOM objects to the information-consuming enterprise, or having to reconcile the data to local identifiers or terms.

This is an efficient way to “browse” imaging data managed by an outside system and organization, but is often not efficient if advanced processing is required (if the image viewer lacks the features) or if the imaging data need to be closely compared to data stored in other systems (like the local PACS). While this method may suffice for some clinicians, Radiologists likely prefer the data to be presented in their primary system (linked to the local Patient ID and all other imaging records): the PACS.

Guest Studies

In some cases, the DICOM data is moved to the local PACS and stored temporarily. These data are available for viewing using all the PACS tools, but are not stored to the long-term archive. The system purges the data from the PACS cache based on any configured retention rules. These exams are often reconciled to local identifiers, like the local enterprise’s Patient ID, to make comparison in the system easy, but not all organizations will localize these data (see note below).

Many organizations will apply a specific labelling, such as a prefix or suffix character or string in the Study Description, to denote that the exam was acquired elsewhere. This can preempt any confusion if the acquisition protocol or image parameters are not consistent with the local policies. When used consistently, this method may also help identify the number of imported exams within an imaging IT system.

This approach is common where images are shared with an organization, through an image sharing solution or portable media, and the local PACS is the preferred viewer (due to its advanced tools and/or system familiarity). It is also used where Radiologists need to review the imaging data for scenarios like teleradiology or consults, but the patient is not being transferred or admitted to the local organization.

Archived Exams

Like Guest Studies above, these exams are received, stored, and (typically) reconciled to include local identifiers (for example, Patient ID and Accession Number) and terms (for example, an updated Study Description). They are archived to the PACS or VNA and made part of the local enterprise’s patient medical record.

This is common where the patient is going to be transferred to the local enterprise or will be getting diagnostic or clinical services, such as a follow-up imaging exam or surgery, and the enterprise wishes to retain these records for future reference.

Notes:

- Documented organizational policies and procedures that define when and how outside imaging exams are accessed and imported should provide guidance to staff and affiliates.

- Determining whether an outside exam is beneficial or necessary to import requires significant knowledge. Often, a Radiologist is required to make this decision, but in some cases an experienced imaging analyst with deep Radiology knowledge, like a senior Technologist, may be able to make this determination in many cases.

- For Guest Studies and Archived Exams, if the data are not reconciled to local identifiers, there are some risks that the outside identifiers match local ones, which can result in a potential patient risk (exam linked to wrong patient). It can also cause issues when searching for data (some demographic values as stored in the DICOM data need to be known), resulting in some clean-up activities during a data migration.

Exam Counting Methods

Many vendors run a query against the imaging IT system to collect a count of all imaging exams stored to the system over a period (for example, a year). They count each exam that has a unique Study Instance UID value (a required DICOM attribute). This method would include all stored exams, including imported exams.

Another method is to have the health system produce a report from their RIS that provides a count of all imaging exams performed by that enterprise. This list could exclude imported exams and would generally represent exams for which the health system received revenue in the form of TechFees. The vendor would have to trust the health provider’s report, but a sanity check against the imaging IT system’s database would suggest if the information were within reason.

How Much Difference Does this Make?

So, is this aspect worth looking into? Let’s look at some numbers.

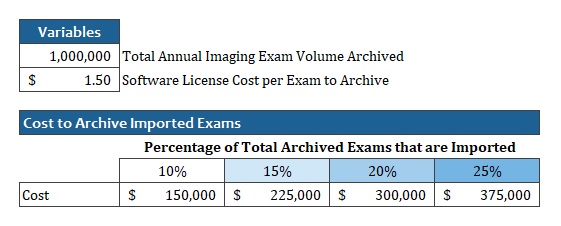

Imagine a large healthcare enterprise that stores a total of 1 million imaging exams to their PACS each year. As an academic system with lots of affiliations, this enterprise has many patients in the area routinely referred for additional imaging and treatment.

Their vendor charges $1.50 per exam stored to the system.

If we assess different percentages of the total exam volume that is imported, we see that the cost to store imported exams could vary from $150K to $375K.

Keep in mind that the health system has no TechFee revenues to offset these costs (though there may be other clinical or diagnostic services that the patient receives for which the health system can bill).

The Model Matters

In the above case, if the vendor licenses the software based on a total number of annual exams, as long as the total annual exams stored does not exceed the amount currently licensed, no additional software license needs to be purchased. If the vendor counts imported exams in the total, and image sharing increases, it may require the health system to purchase additional licenses (for example, to allow another 50K to 100K annual exams to be stored), even though they receive no revenue for the imported exams.

If the vendor licenses the imaging IT solution on a per-exam usage fee, and they count imported exams, the health system would have to pay the vendor for each exam imported (at whatever rate they specify in the agreement, which may be the same as an acquired exam, or at a lower rate).

Other Costs and the Cloud

Today, most healthcare providers procure and manage their own hardware (for example, servers, storage, and network equipment) and the solution vendor supplies the software, technical and professional services, along with ongoing support. So, in addition to any software license costs paid to the imaging IT vendor, the health system also must supply the hardware to store and manage the imported exams, and the labor to perform the importation. If a data migration is performed sometime in the future, the health system will have to pay for any imported exams that are included in the migration.

This is all in addition to any fees paid for an image-sharing solution.

The above details are important to consider if a cloud-based PACS solution is considered.

When a system is on-premises (for example, hosted in the health system’s data center), the vendor may be willing to acknowledge that the imported exams do not count towards the total exam volume when calculating the software license, but when they also provide all the hardware infrastructure, they will incur costs for all data stored. This may result in some fee being charged to the health system.

Sidenote: Enterprise Imaging

While beyond the focus of this article, many of the same questions should be posed when storing clinical images, also called Enterprise Imaging (EI) content, to the imaging IT system. Most of these data sets are not captured in response to an ordered service and have no billing associated with their capture or storage. If the imaging IT solution vendor counts these data sets (which may be one or more image, video, audio file, document, etc.) as an exam when determining software license compliance or system usage, costs (with no associated revenues) could be higher than expected.

Sidenote: Labor for Importing and Reconciling Exam Data

Another significant cost of image-sharing is the labor involved in reviewing, importing, and reconciling the imaging data to use local identifiers. This cost is not hidden, but is not measured by most enterprises, and these costs can be larger than many people understand. Industry vendors have worked on solutions to auto-generate the necessary order information to perform reconciliation automatically. New data standards, like HL7 FHIR® (https://www.hl7.org/fhir/), and APIs that support them developed and deployed in EHRs make this approach more feasible. Careful attention needs to be paid to how data elements like Study Description are applied in the reconciled data, as how procedures are labelled vary among enterprises. Inconsistent Study Description values can affect relevancy rules for pre-fetching and routing and may necessitate maintaining complex terminology mapping tables (if supported by the imaging IT solution). Series descriptions, which often affect features like display protocols, also vary among modalities and enterprises. Terminology normalization is a complex challenge involving many unmanaged data variables that some believe may be solved more effectively through the application of Artificial Intelligence (AI).

Tips for Minimizing Costs

The first step is understanding your current situation with the following factors to consider:

- Do an inventory of acquired (check the RIS) and imported exams for each year for the past three years. Understand how many exams you are importing (with no offsetting revenue) and look for any trends. Are exam imports increasing year-over-year?

- Read the agreement with your current vendor to understand the terms around how exams totals are counted. Understand whether they differentiate between acquired and imported exams. Understand whether Guest Studies (as described in this article) are counted, even though they are not archived.

- If your imaging IT vendor does count imported exams when calculating the software license or usage, make sure you account for these costs when budgeting capital and operating budgets.

- Understand the fees for any image-sharing solution you use. Does the vendor charge a different amount for exams that are viewed from the cloud, but not imported to the local PACS? Do they charge both the sender of the data and the receiver, or just one of the parties?

- Review your policies and procedures for exam importation. Are they clear so that the necessary exams get imported, but ones that are not relevant are not?

If your organization is looking to replace an imaging IT system, like a PACS or Vendor Neutral Archive (VNA):

- Ask the bidding vendors how they determine which exams are included in the count for software license calculations. If some do count imported exams and some do not, include an estimate of the additional costs for those that do in your Total Cost of Ownership (TCO) analysis.

In Conclusion

The purpose of this article is not to dissuade enterprises from sharing imaging exam data. As stated, there are many benefits of this activity to all stakeholders, most notably the patient. The purpose here is to explore variability in how imaging IT solution vendors count exams for software licensing, and how this can add up to represent significant costs, over time.

It would be unwise to select a new imaging IT solution simply based on whether they count imported exams toward the software license or not, but it should be considered in your cost projection calculations.

And it may be worthwhile to educate your imaging IT vendor partner on the economics of providing diagnostic imaging services and to align their compensation to reflect the scale of the enterprise’s revenues.