I have been reading a lot recently about trends in healthcare and imaging around costs and revenues. There seems to be a perfect storm of changes in the market that will have a fundamental impact on diagnostic imaging service providers. I find this topic interesting because, unless you understand how the money is moving, you won’t understand why things are happening. Here is a summary of what I have discovered.

Medicare Reimbursement Cuts

This one is obvious. If you lower the amount of money paid for something, your revenues will go down (unless volume goes up proportionally). Here is an infographic from MITA on the cuts made since 2006.

Fewer Medical Imaging Exams being Ordered

Here is an article from MITA on the decline of the total number of CT exams being done in the U.S. Here is another one citing data published by the American College of Radiology (ACR). It states: “…physicians are calling for less, not more, imaging tests.” This shows a measurable reduction in the volume of exams performed in the U.S. And here is an article indicating a steady decrease in imaging studies being ordered for patients in the ED, following a steady increase up to 2007.

Image Sharing

The sharing of patients’ clinical records across facilities is a key part of Accountable Care, and is generally a good thing for patient care. So is sharing imaging records. With reliable options now available on the market, sites within a local referral area are rapidly launching or signing up to services to share images. The clinical benefits of comparing new imaging exams with priors are well understood, but this practice will often result in avoiding the need to perform a repeat exam. This benefits the patient (less radiation and anxiety and delay), and the operations of the receiving organization (less schedule disruption, less costs due to CD importation). The other impact, of course, is that the receiving organization loses some revenue from that avoided repeat exam. This will result in a reduction in volume of exams performed.

Adoption of Clinical Decision Support

Starting on January 1, 2017, imaging exams will require the use of Clinical Decision Support (CDS) to ensure that physicians are following Appropriate Use Criteria (AUC). In addition to clinical evidence, factors such as relative radiation level and cost of the exam are used to determine what is appropriate. All things being equal, the lower cost exam is likely to be recommended. The adoption of CDS may result in a reduction in volume of exams performed, or a recommendation to a lower cost (profit) exam.

Preauthorization Requirements

In some insurance plans, preauthorization is required before certain exam types can be ordered (even when CDS is used, in some cases). This may require a consultation with a radiologist or Radiology Benefits Management (RBM) company. Here is an article from 2011 on the use of preauthorization and CDS. The larger the burden on the ordering physician, the less likely they are to order the exam, which may result in a reduction in volume of exams performed, or a recommendation to a lower cost (profit) exam.

Patient Steerage

Last year, I did a blog post on an article on the trend of “patient steerage”. The original article is here. Essentially, patient steerage is when a payer incents a patient to use a provider that offers the imaging service at a lower cost. If a service provider is not price competitive, this will result in a reduction in volume of exams performed.

The Castlight Effect

This company received a lot of attention because of the size of its IPO, but it is also notable for what they actually do. As this article explains, they provide healthcare provider cost information for a range of healthcare services to employee health plans. The intent being that, given the choice, consumers will choose lower cost options. This is very likely to happen when the patient has a significant co-pay (e.g. 20%) and they will personally benefit from lower cost options. If a service provider is not price competitive, this will result in a reduction in volume of exams performed.

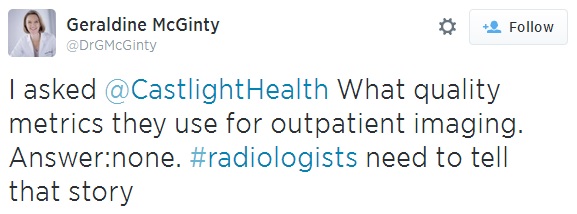

Wait, but what about Quality?

With all the talk about the shift of reimbursement from volume of procedures to quality or outcomes, I found this tweet on Castlight interesting…  If we shift away from volume incentives/payment, reduce the prices paid (through policy or competition), but don’t recognize quality, the service of diagnostic imaging has been commoditized, and I don’t think that this will benefit patients, in the end.

If we shift away from volume incentives/payment, reduce the prices paid (through policy or competition), but don’t recognize quality, the service of diagnostic imaging has been commoditized, and I don’t think that this will benefit patients, in the end.

Consolidation

I have heard a couple of opinions that believe that the strong trend of consolidation among healthcare providers will allow the largest of providers to dictate terms and pricing to payers. As it was explained to me, it works like this: The big, well-known healthcare provider, which has bought up many of the facilities in the area, tells the insurance payers, ‘If you don’t give me preferential pricing for my services, I won’t accept your insurance plan at my facilities’. If the healthcare provider is big enough and well respected, the insurance provider will have a tough time selling insurance plans to companies and individuals when the buyer learns that they can’t go to the big provider. This is called leverage. If this is true (and I think that it is), this will result in isolated areas of reimbursement stabilization or even increases. Here is an article talking about what the impact of provider consolidation means to private payers. It cites a steady increase in the number of physicians becoming employees of hospitals (vs. independent private practices)…

“…the number of doctors employed by hospitals increased to over 120,000 from 80,000 between 2003 and 2011. About 13 percent of all doctors are now employed directly by hospitals.”

A Necessary Change in Revenue Cycle Management Systems

Here is an article on the need for an overhaul of Revenue Cycle Management (RCM) systems in the U.S. It includes some stats on administration costs per transaction (compared to financial services transactions) and consolidation trends, as well as the value of analytics. Some excerpts…

“…the number of hospitals per integrated delivery system took a big jump last year from 6.4 to 7.1…”

“…the physicians who go into practice do not want to be entrepreneurs as much as they used to. When 52 or 53 percent of residents today become employees of integrated delivery systems, it tells you that the whole market has changed.”

Using Analytics to Maximize Revenues

Here is an article on using analytics and their reports to optimize financial operations.

So, what do you think?

P.S. Here is an interview that goes into the details of payer vs. provider, along with a case for more bundled payments. And here is a blog post that goes into more detail on bundled payments, including the shift from retrospective to prospective bundles.

P.P.S. Here is an article explaining the difference between charges and costs.

P.P.P.S. Here is a notice of rule changes proposed by CMS on the method by how physicians fees will be determined. “…we are updating our practice expense inputs for x-ray services to reflect that x-rays are currently done digitally rather than with analog film.”

P.P.P.P.S. Here is an article on a study on the disparity of costs for a Mammogram in the L.A. area. $60 to $254 for self-pay, with a bill of $694 to the insurance company for the same procedure elsewhere. 30% of Mammograms in the study were self-pay.

P.P.P.P.P.S Here is an article, with a nice infographic, on 5 common medical practice denials and remedies. Spoiler alert: Radiology made the Top 5 list of unexpected denials.

P.P.P.P.P.P.S Here is an infographic on the declining employment demand and income of Radiologists by a medical recruitment firm.